10 years ago an insured person would expect higher returns on any money they invest for retirement than they would today. The mandatory interest credit for Swiss pension plans according to BVG/LPP was 2.50% in 2007 compared to 1.00% today. Ten-year Swiss government bonds yields have fallen from 2.6% to -0.1% in the same period. This not only affects expected returns on the assets set aside but also the cost of providing an income for life after retirement. Life expectancies for retiring pensioners have increased by about 1 year for females and 2 years for males in that time which also needs to be funded.

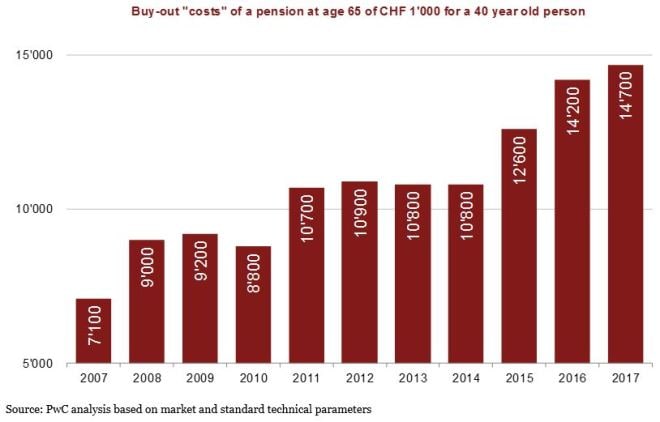

All of these factors have had a major impact on retirement outcomes. Based on our calculations, in 2007 a 40 year-old could invest CHF 7’100 and expect a pension of a CHF 1’000 a year for that investment. Today a 40 year-old would expect to have to invest CHF 14’700 – more than doubling of the cost of retirement over 10 years. In that time, inflation expectations have also fallen, but overall the cost of retirement has increased.

What can pension funds do?

Pension funds aim according to our experience to maintain the level of retirement benefits they provide while financing the promises already made. But pension funds are in a “zero-sum” game – without extra funding, members will ultimately receive lower benefits on average when results are not what was expected. Robust analysis and forecasting of what employees can expect to receive, combined with clear communication may be the best what they can do. Other measures are down to employees and employers as recipients and sponsors of retirement benefits.

What does this mean for individuals and employers?

Find higher returns? In conventional collective Swiss plans, employees share in the overall returns of the fund as they are credited to them. This limits opportunities to take more risks, with an expectation of higher returns. For higher earnings, it is possible to have individual strategies through a “1e” pension plan. These plans can be used to seek higher returns, but this may not be suitable for all.

Later retirements? Without saving more, employees have to retire later for the same outcome. In some ways this is only reasonable: If life expectancies increase without changing retirement ages, the proportion of life we spend in retirement rises. Employers may have to prepare for the ageing effect on their business – not only their workforce recruitment and retention, but possibly their business strategy and target markets.

Employers pay more? One answer may be employers paying more. But employers face economic challenges themselves, with increasing competition and pressure for results. For most companies, raising costs or investing cash may not be palatable.

Employees pay more? Creating more awareness of the individual options available for the employees is one option. Additional voluntary employee contributions are typically deductible for tax purposes. Some employees don’t have confidence in their pension plan and are not keen to lock away money until retirement.

How can companies create further incentives for employees to pay more? A look abroad could help.

Could “matching” be part of the solution?

In the US as well as the UK, contribution “matching” is widely used in pension plan design. Employer contributions are adjusted to “match” those of employees. When an employee contributes a percentage of their salary into the plan, the employer contributes an amount directly linked to what the employee pays. This could be 1:1 – i.e. if the employee pays 2% of pay, employer pays the same. Or some ratio like 2:1 or 1:2.

The big advantages of matching are two-fold: it encourages employees to pay more; and it focuses employer spending where it is most valued by its employees. One of our clients challenged the common Swiss plan option of employers paying the same for all employees, whereas employees can choose their level: “Why can employees choose to pay less, but I cannot follow when they do?” A reasonable question that matching helps to address.

The challenge is that legislation in Switzerland currently restricts the ability to apply matching within the regular plan. The law requires the employer contribution rate to a pension plan to be the same for all employees in the same situation (e.g. age, grade etc). “Matching” can be done through the buy-in system. So with the right plan design, matching can be incorporated within the Swiss plan.

This won’t for every situation as the use of buy-ins is subject to certain caps and restrictions which may become a barrier. Plan administration may be more complex. But in challenging times for pension outcomes, new solutions may be needed.